Conferences Grew Nearly 30% in 2022 But Sell-side Conferences Barely Budged

Sanford Bragg

Integrity Research Associates, LLC.

Conferences came roaring back in 2022, but bank=sponsored conferences grew less than 2%,

according to data supplied by investor relations platform provider Virtua. Physical

conferences resumed and virtual conferences waned.

More conferences

The number of conferences in 2022 tracked by Virtua’s StockConferenceCalendar service

increased by 29% from 2021, achieving the highest level over the last six years. In

contrast, bank-sponsored conferences increased only 1.7% as many banks constrained their

corporate access programs. The market share of bank-sponsored conferences shrank to 33% in

2022 from 45% the prior year.

Credit Suisse surpassed rival UBS as the top conference organizer among banks, as UBS

radically downsized its conference sponsorship from 205 conferences in 2021 to 97 in 2022.

Third-ranked Citi cut back more modestly, reducing its conference sponsorship by 16%.

Some smaller investment banks, such as Redeye Capital, Stephens, and Sanford Bernstein,

aggressively expanded their conferences in 2022. Fourth-ranked Jefferies also upped their

conferences to 70 in 2022 from 48 in 2021.

In contrast, many of the bulge banks dialed back. Besides UBS and Citi, JP Morgan and Goldman

both reduced their conference sponsorship.

Only a few more bank sponsors

The overall number of conference sponsors increased 14% in 2022, from 388 in 2021 to 442. The

number of non-bank sponsors increased less than half that rate (6%).

Favorite locations

The number of virtual-only conferences shrank nearly 40% in 2022, as physical conferences

once again became the most popular form.

New York and London resumed as most favored physical locations while Singapore displaced Hong

Kong as the most popular Asian venue. Seven of the top fifteen venues were located in North

America.

The analysis is based on data supplied by Virtua StockConferenceCalendar, considered to be

the largest global database of investment conferences and presenters. Virtua is a financial

services technology company focused on providing platform-based analytical tools and

services tailored to the workflow needs of Investor Relations (IR) professionals and

publicly traded issuers. Although the firm is headquartered in Boston, much of the analysis

and data collection is done in India.

Virtua, which provides platform-based analytical services for Investor Relations (IR)

professionals, acquired StockConferenceCalendar in 2015 from Dremer IR Counsel, an IR

consulting

company.

Our Take

Although virtual conferences are no longer the norm, they won’t be going away. Their

advantages

of convenience, global reach, and reduced travel costs are supplemented by greater ease in

organizing, which means that virtual conferences will continue to be popular for topical

events.

Nevertheless, virtual conferences can’t fully replicate the networking offered by physical

conferences. After two years of Covid isolation, demand for physical conferences was

overwhelming. Perhaps successive years will balance out virtual and physical conferences

more

evenly.

ShareSubscribe

Dec

14

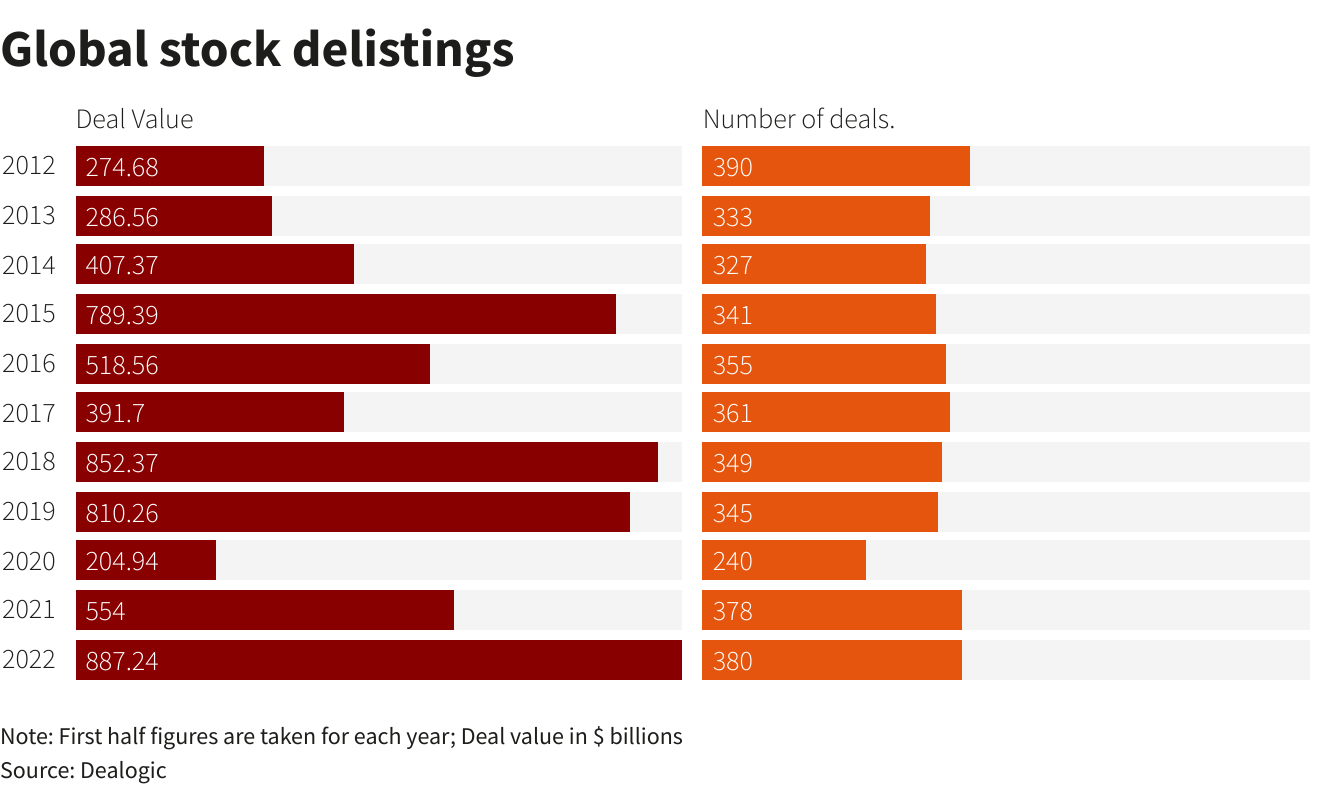

Understanding Take Private Transactions

And trends to identify them before they go down

CJ Gustafson

Author Designation

Have you ever heard of a company being taken private? Coupa is the latest example of a big

name being de-listed from a stock exchange and purchased by a private equity buyer.

It's becoming increasingly popular for companies to go private, especially when they are

trading at “attractive” prices. So what exactly does a take private entail? And why does it

happen?

The What

A take private is a transaction in which a publicly-traded company returns to private company

status, generally as a result of a sale to one or more financial buyers. The buyer could be

a

strategic (Salesforce buying Slack), a private equity firm (Thoma Bravo buying Sailpoint),

or an

eccentric billionaire (Elon Musk buying Twitter).

Continue reading...

The Why

There are many reasons why companies might choose to go private. One of the main benefits is

that

the company is no longer subjected to the scrutiny of being a public company. It’s tough

being

in the lime light. There are a lot of expectations around performance.

As a private company you can generally operate with less transparency, which can allow you to

make decisions more quickly. This can be beneficial if the company wants to pursue a

strategy

that might not be popular with investors, or take a long time to materialize, such as a

re-org.

Going private can also allow the company to take on greater debt, which in turn can provide

more

money for growth or other purposes.

Finally, taking a company private can allow the stakeholders to reap the benefits of a

company without the cost of keeping everyone up to date. The administrative burden that goes

along with reporting quarterly results is huge. There are entire departments of people at

public

companies focused legal and communication.

Real World Examples

Some of the most well-known companies that have been taken private include Dell, Toys R Us,

and

Burger King.

In 2013, Dell announced that it would be taken private in a deal worth $25 billion.

Toys R Us was taken private in 2005 in a deal worth $6.6 billion.

Burger King was taken private in 2010 in a deal worth $3.3 billion.

At the top of this post is a larger sample from the tech world, which we used in the analysis

below.

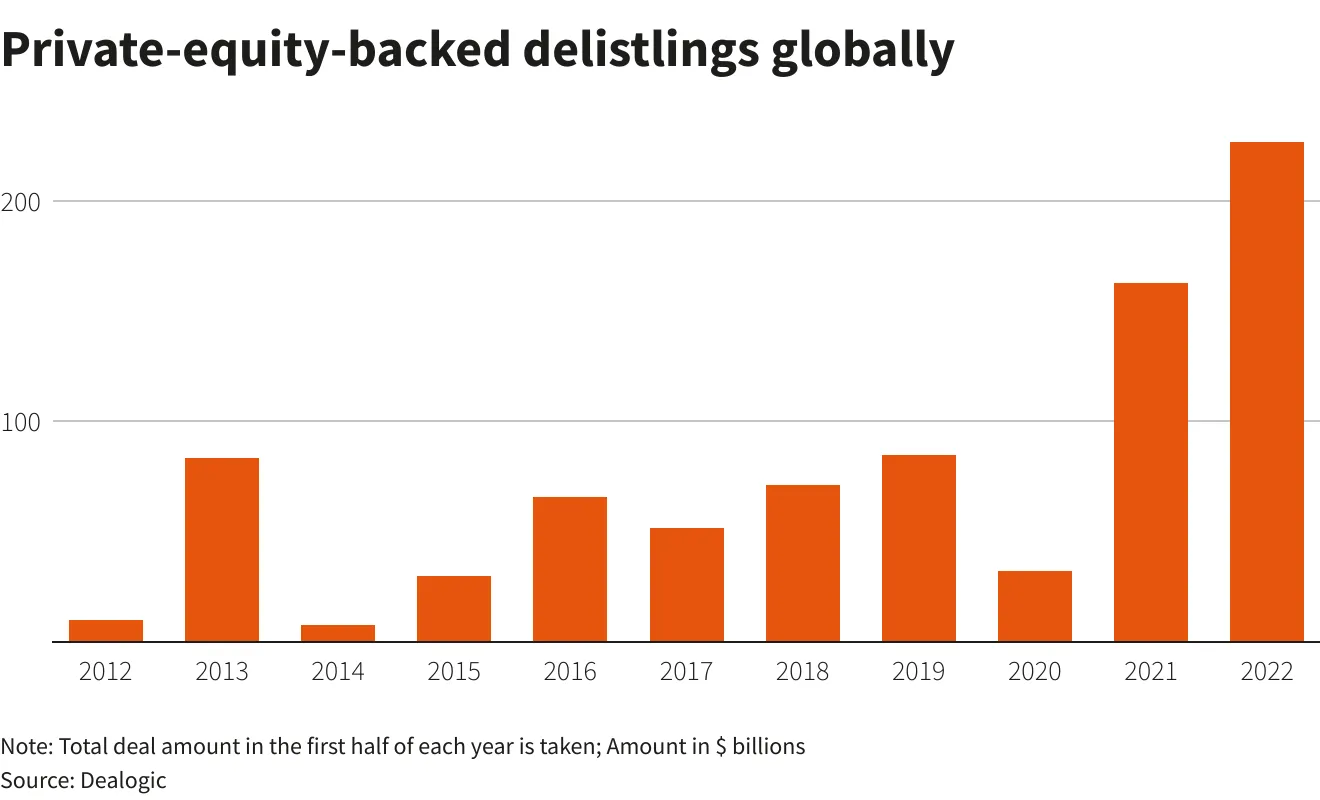

Private Equity Players

Private equity firms are often the ones that take companies private.

Some of the most active private equity firms in this area include Thoma Bravo, Vista Equity,

KKR,

Carlyle, and TPG Capital.

Together, these 5 firms have been involved in some of the biggest take private transactions

in recent years.

Leading Indicators

I teamed up with our friends at Virtua to investigate the financial profiles of

companies in the lead up to being taken private. They crunched the data from 50 tech take

privates over the last decade using their powerful lifecycle analysis tool.

The charts below represent Take Private company performance vs Tech Sector performance, with

Q = 0 representing the time of being taken private. This neutralizes for whatever the market

volatility was at the time (also known as financial benchmarking voodoo).

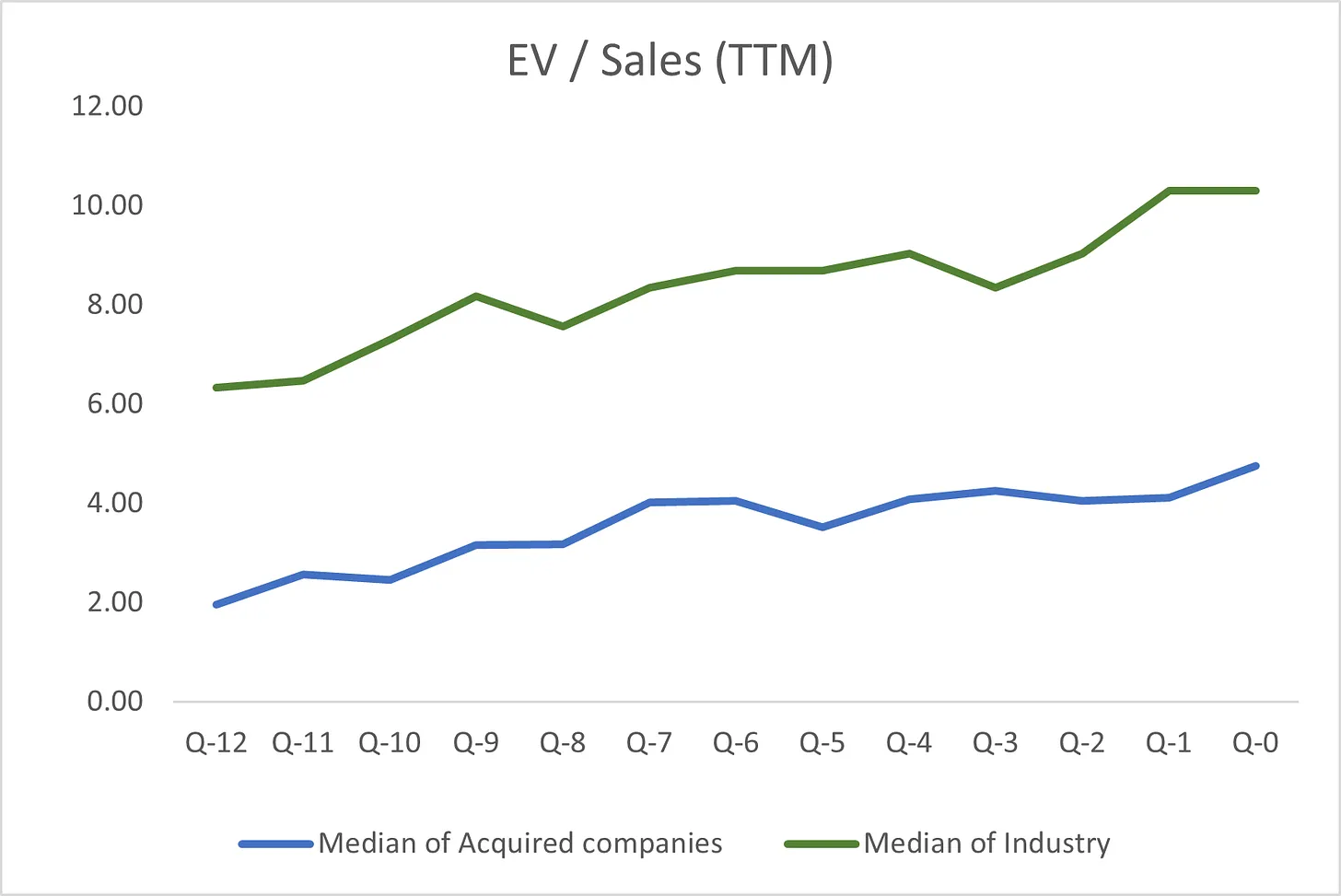

Signal #1: Lower EV / Sales

As a reminder, EV / Sales = Enterprise Value / Revenue

Enterprise value is calculated as market cap plus its debt (total debt) less any cash

and

cash

equivalents

From an investor perspective, higher value of EV/Sales can be indicative of the

“expensiveness” of the valuation of the company

Conversely lower EV/Sales ratio is considered better investment opportunity as the

company is

considered

undervalued (in relationship to its peers)

A low EV / Sales may also indicate lower growth expectations, while a high EV / Sales

may

indicate

that

investors expect big things (and big growth)

Takeaway: Companies with lower growth are in the cross hairs (single digit to high

teens);

especially

those who were growing REALLY fast and slowed to medium fast

Signal #2: Lower EV / EBITDA

Generally, the lower the EV-to-EBITDA ratio, the more attractive the company may be as a

potential investment, as it spits out cash

A low EV-to-EBITDA ratio could signal that a stock is potentially undervalued

A lower EV/EBITDA means you're spending less money for a $1 of earnings. So that's a

good

thing

Takeaway: Investors pony up for profitability, especially when it’s cheap.

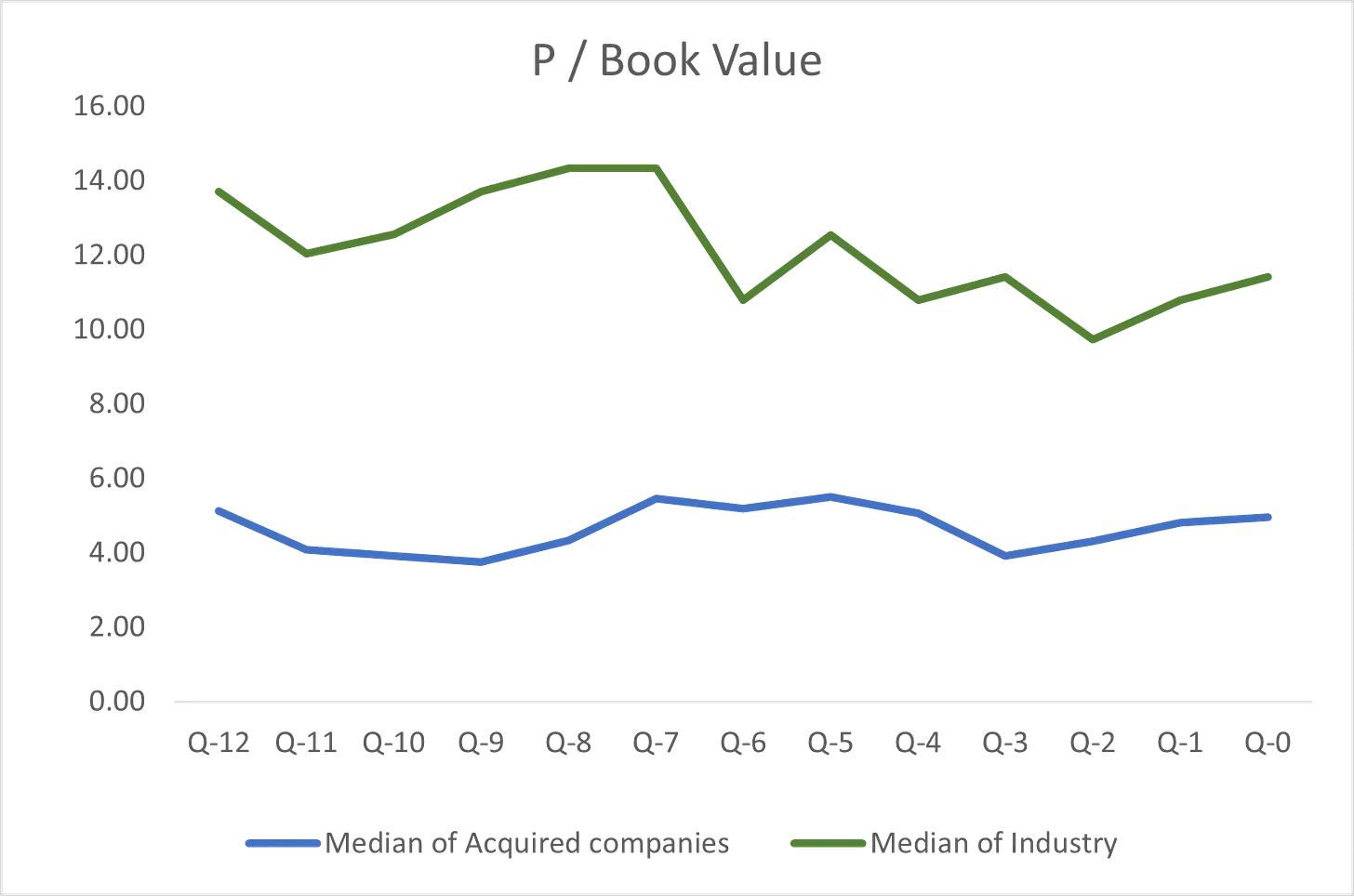

Signal #3: Lower Price to Book Value

Investors use the price-to-book value to gauge whether a company's stock price is valued

properly

A P/B ratio of one means that the stock price is trading in line with the book value of

the

company

A P/B ratio with lower values signals to investors that a stock may be undervalued

In other words, if a company liquidated all of its assets and paid off all its debt, the

value

remaining

would be the company's book value

Takeaway: The P/B ratio provides a valuable reality check for investors seeking growth

at a

reasonable

price

Who Could Be Taken Private in 2023?

Potential names that have been floated include Peloton, Shake Shack, and AMC

Entertainment.

The biggest potential headwind for take privates in 2023 - the cost of debt. Many take

privates are financed with a heavy dose of debt. In fact, Twitter owes at least $1B annually

in interest payments on the $13B in debt required to take it private.

But then again, rising interest rates do contribute to the stock market dips that make take

privates a lot more appetizing… soo….

But, if I was a betting man (disclaimer: this is not financial advice, I just have a

degenerate streak and like to watch the ponies run from time to time), I’d say

SumoLogic.

My buddy Matteo writes “Work3” - a weekly column on the changing nature of work.

He interviewed me on my career journey, starting Most metrics, and where I see the “future of

work” going. Spoiler alert: I think people will increasingly see their networks as the

businesses they work for, not the C corps themselves. More in the link below:

I’d recommend you give Work3 a subscribe for a fresh take on workplace evolution.

Quote I’ve Been Pondering

Every culture has its own way of teaching the same lesson: Memento mori, the Romans

would remind themselves.

Remember you are mortal.

-Ryan Holiday, The Obstacle is the Way

ShareSubscribe

Nov

22

Mostly made up: Growth adjusted gross profit per employee

I made up a metric

CJ Gustafson

Author Designation

First off, thanks to everyone who joined the “Mostly talent

collective”. We had over 50 people join in the first week 🤯. The collective now includes candidates from companies like PwC, Bain, and McKinsey, all looking to join high growth startups🧠.

So, of course, I had to take the good boy for ice cream🍨 to celebrate.

Mostly metrics’ editor and chief: Wally

If you’re an employee looking for your dream job, you can get on board 👇🏾

Now on to the meat🥩and potatoes🥔 of today’s post - I teamed up with my friends at Virtua

Research to bring a metric I’ve had bouncing around in my head for a couple of years to life.

It’s called Growth Adjusted Gross Profit per Employee.

Continue reading...

Here’s how it works:

Take a company’s Gross profit (Revenue less Cost of Goods Sold)

Divide that by the number of employees they have on board (total headcount)

Multiply that by (1 + y/y revenue growth)

Here’s an example comparing two fictional companies:

Step 3: $83K x (1+ 60%) revenue growth rate = $133K

per Employee

Company A comes out as the more efficient operator, and a potentially better bet. Even

though Company A isn’t growing as fast as Company B, it has a healthier gross margin and

is generating more Gross Profit per employee.

With that example under our belts, let’s get familiar with the formula’s components and

why they’re important.

Gross Profit:

At the end of the day, the higher your gross

profit, the

more money you have to run the rest of the business.

A gross margin of 74% (a rough median for software companies) means that for

every $1 the biz brings in, 74 cents is left over for salaries, rent, and other OPEX

(including those ugly laptop backpacks they give out each year at your company sales

kickoff).

Margins matter - take it from my friend Kyle Harrison, who dove into why Twilio is trading at a MASSIVE discount to other high growth SaaS companies like Atlassian and DataDog:

So when companies like Datadog and Atlassian are trading at ~10-15x revenue, why is Twilio down at ~1.5x revenue?

In part? Gross margins.

Remember that Twilio has ~50% gross margins.

Datadog? 77% Atlassian? 84% Cloudflare? 78%

Right out of the gate, that $2.8B in revenue? It’s

costing Twilio ~2.5x more to get it.

I believe we should STOP talking so much about revenue multiples and START talking more about multiples

of Gross Profit.

Why?

Well, as a friend of mine likes to say:

“I love Revenue, but if I fed my dog Revenue, he’d

die. He needs Gross Profit to survive.”

Gross Profit is the lifeblood of any business. Companies can’t just trade a dollar for a

dollar forever (unless it’s the Costco $1.38 hotdog).

Now, with that being said, you might say why don’t we just look at profitability?

I don’t want to over rotate and only size up companies based on their profitability. I think that too misses the forest through the trees when

you are talking about high growth tech firms.

EBITDA multiples are cool, but there are times when you are chasing a market opportunity and it makes sense to burn cash, IF you can still protect your gross margin, which will eventually be your route to scalability. Tech markets come with windows of opportunity, and the difference between being #1 vs #2 in a market is huge.

Gross Profit per Employee

This is a remix of one of my favorite metrics, Revenue

per Employee

Revenue per employee is a simple metric that cuts through all the noise

There’s no hiding from it - just take the amount of revenue you’re generating and

divide it by the number of people on board

This should go up over time, and demonstrate

leverage in your business model.

With Revenue per Employee, ideally you get close to $250K or $300k per person

when you approach $100M in revenue

So for Gross Profit per Employee, ideally you get into the $200K to $250K range

as you approach scale (on an annualized basis)

This is something companies should track closely to make sure they aren’t getting

out over their skis with hiring during hyper growth

Revenue Growth Rate

Best measured on a TTM (trailing twelve month) basis

No matter how you slice it, high revenue growth covers up a lot of sins

The question this formula assess is… just how many sins?

So what’s the point?

The point of this formula is to balance business model

scalability (Gross Profit) with operational

leverage (Gross Profit per Head) and ability to execute on

the sales side (Revenue growth rate).

When I look at a company to work for, advise, or invest in, I want to have faith in where

they’re going. I’m very willing to accept that not all companies will be profitable

RIGHT NOW.

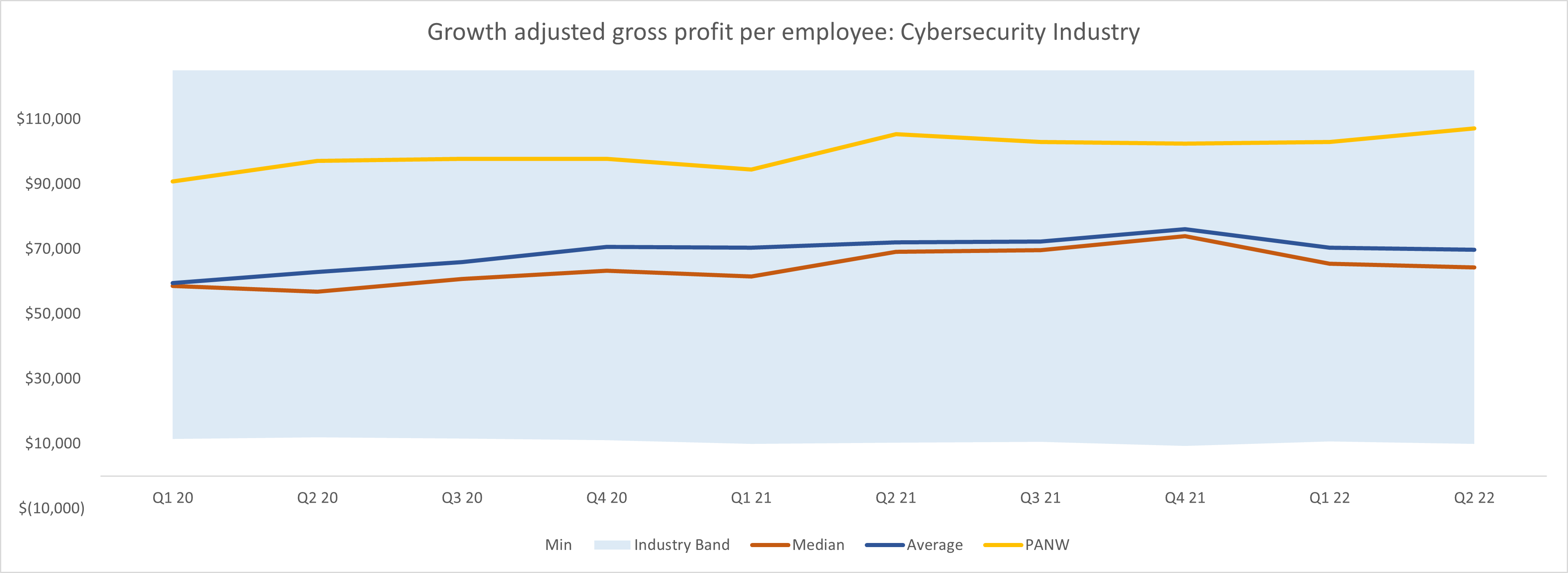

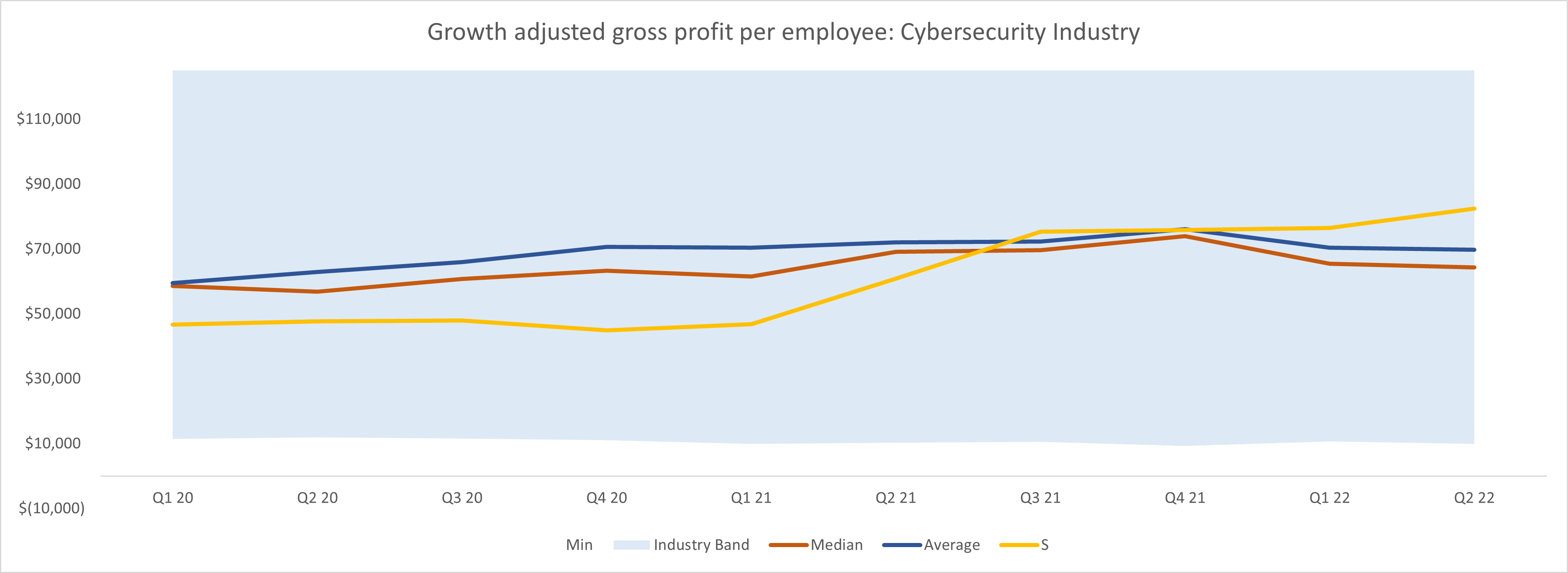

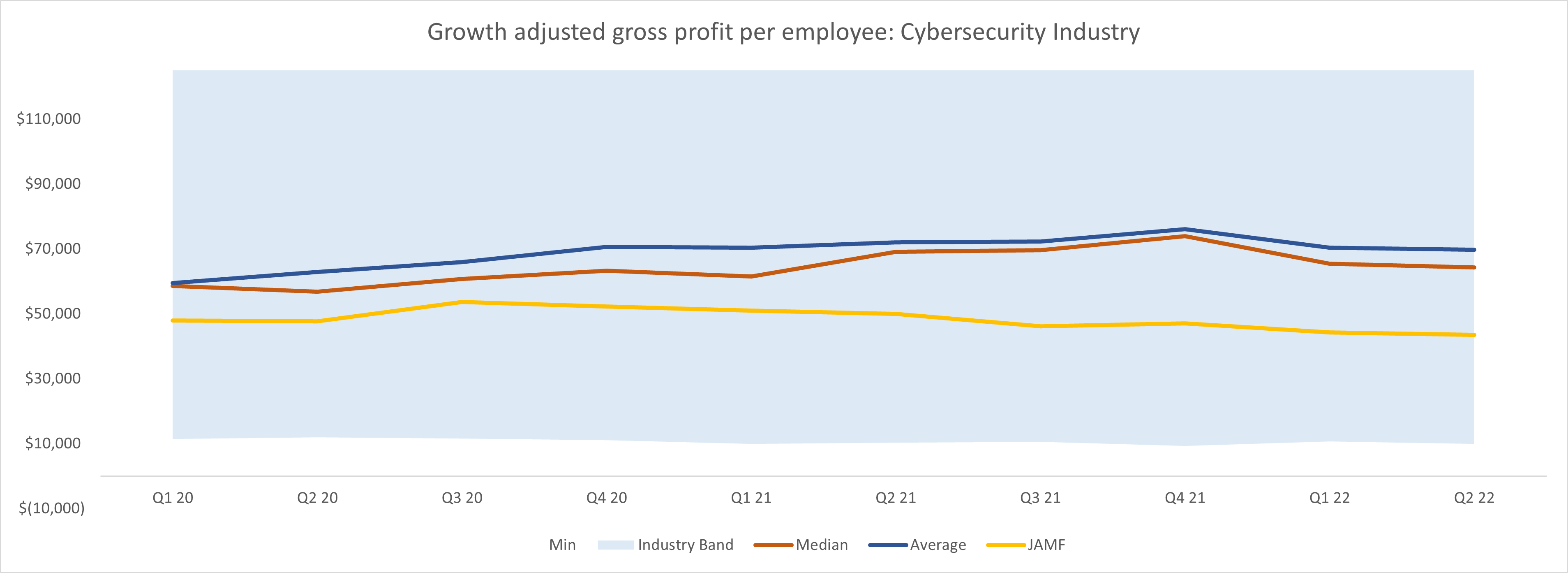

Here’s Crowdstrike ($CRWD) vs their Cyber Security sector cohort. You can see they are

generating $15K to $25K above the industry median and average. It makes sense why

investors are willing to pay a premium - not only is their Gross Profit healthier than

most, they are generating it with a sensible number of employees on board, and growing

faster than the sector. A few more examples…

A(nother) cybersecurity company outperforming: Palo Alto ($PANW)

A cybersecurity company on the

rise: Sentinel One ($S)

A cybersecurity company underperforming: JAMF.

Putting it to use

This metric, in my (made up) opinion, is best used to compare high

tech growth companieswho are later in their lifecycles

(+$100M ARR, post series C, or post IPO) with similar

monetization models.

I think it’s also interesting to not only compare companies vs one another, but also

check how a single company is trending over time - are they getting better at what they

do?

I’m going to start tracking Growth adjusted gross profit per

employee as my own personal “index” of sorts.

As a metrics wonk, it combines three of my favorite signals into one. I think looking

purely at revenue multiples quarter to quarter is misleading. You can still go fast and

grow like crazy, but have a rotten core that’s ripe for burn out.

And I don’t think we should only care about profitability. Like, how boring is that? If

you want slow growth and high profitability, go buy a car wash or dry cleaning business.

(I joke, I joke, I joke).

So there it is - Growth adjusted gross profit per employee.

Next time we revisit this metric we’ll size up the DevOps industry to see how companies

are performing.

What I’ve been reading

As a business leader, you have a few big decisions that will 10x your growth or sink your

business.

That’s why I’m a big fan of Brian and his newsletter. Every week he shares simple tips to help you make the big choices that grow your business.

Join 7,000+ business leaders and check out The Competitive

Edge to help position your business to grow

“At no point in your rambling, incoherent response were you even close to

anything that could be considered a rational thought. Everyone in this room is now

dumber for having listened to it. I award you no points, and may God have mercy on your

soul.”

-Principal in Billy Madison

ShareSubscribe

Nov

08

Don't let the Rule of 40 rule your company

Why I think the Rule of 40 is lame

CJ Gustafson

Author Designation

This Thursday I’ll be participating in a virtual event OpenView is putting on to roll out their 2022

SaaS Benchmarking Report. I’ve been a disciple of this report for +5 years, having built multiple annual operating plans off of the rich data set. To a CFO or FP&A professional in tech, it’s the holy grail of SaaS benchmarking.

Curt and Kyle at OV crunched the financial and operating metrics of 660

private SaaS companies so you don’t have to.

RSVP for the event and gain early access to the report here👇

In addition to the lucrative appearance fee I’ll be collecting, I also received early access to the data. While thumbing through it, their recent analysis on the Rule

of

40 caught my eye. You may have heard of this metric - like the Undertaker, it’s risen

from the dead during the latest tech market correction.

Wakey wakey, Rule of 40!

At the risk of ruffling some feathers, it’s time for me to come clean - I

think the Rule of 40 is lame. Let’s dig into why.

Disclosure: OpenView did not actually pay me anything to participate, however, I did stop by their office for happy hour two weeks ago and enjoyed two (free) Miller Lites and one (free) cupcake.

What’s the Rule of 40%?

Continue reading...

The Art:

Trying to measure efficiency when you’re losing money can be a mixed bag of burritos. Some businesses raise

a ton of

money so they can prioritize growth at all costs (see:

Gitlab). Other businesses are designed to run like a money printer, spitting

out free cash flow and fat dividends for shareholders (see:

Qualcomm).

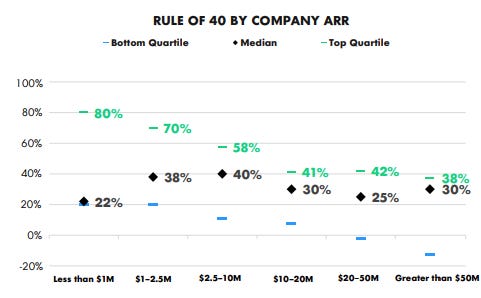

But for many businesses, the truth lies somewhere in the middle. Some investors validate a “good” balance

between growth and profitability by checking if revenue growth rate plus profit (or loss) rate exceeds 40%.

So, if you’re growing at 50% y/y and have a -15% EBITDA margin, your Rule of 40% =

35%…womp womp.

Where does the Rule of 40 go wrong?

I have four bones to pick with the Rule of 40:

It ignores where you are in your business lifecycle.

You can game it with superior growth.

It’s a hard target to keep consistent in all periods, due to seasonality

It’s a lowish bar if you want to be great.

I took a trip in the way back machine using Virtua

Research’slifecycle analysis tool to stress test a cohort of companies in the four quarters leading up to (Q-4 through Q-1) and immediately preceding (Q+1 through Q+4) their IPO (Q0).

The research is based on a selection of 60 PLG companies, in honor of OpenView.

Here are my arguments against a dogmatic

adherence to the Rule of 40:

Thanks for reading Mostly metrics! Subscribe for free

to receive new posts and support my work.

It ignores where you are in your business

lifecycle

WorkDay was a solid investment if you bought in when they went public, and maintains

a strong financial profile to this day. However, their Rule of 40 took a major dip

at time of IPO as they made some investments in the business to scale.

Nonetheless, their stock price jumped 72% on day of IPO. If you religiously followed

the Rule of 40 you would have dumped them, and kicked yourself down the road.

There are times to step on the gas pedal and say damn the

torpedoes. There are also times to get to an efficient

P&L in a hurry. Just because you are in one season rather than another doesn’t mean you are necessarily a “bad” company.

Takeaway: Not all periods are the same. And not all periods should be

40%.

You can game it by going big on just growth

I also think there are diminishing returns past a certain growth rate. Investors aren’t necessarily going to pay any extra for 125% growth vs 110% growth if you are losing 50% per year.

However, adhering to the Rule of 40 in a bubble would give you the vote of approval on growth of 140% and losses of 100%. Talk about false

signals.

Takeaway: Not all growth percentage points are created

equal.

It’s a hard target to keep consistent in all periods, due to seasonality

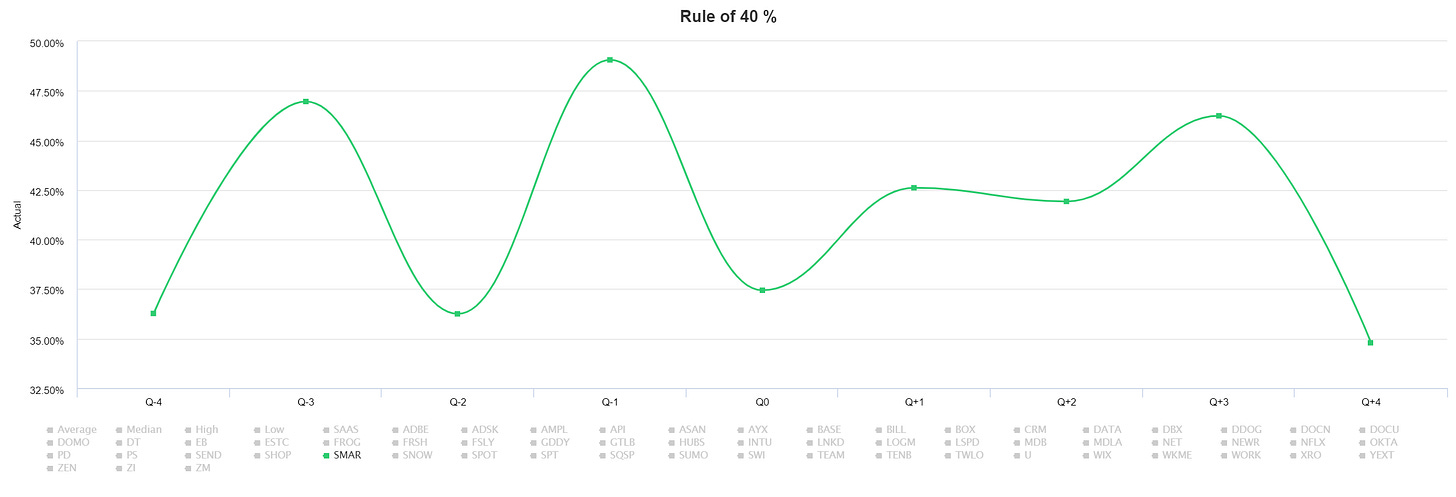

$SMAR Rule of 40

Here’s SmartSheet. They oscillate between a low of 35% and a high of 48%. It looks like one of those Inflatable

Whacky Willys at the used car markets.

I highly doubt when they touched 35% their CEO yelled “HALT THE PRESS! We must get

back to 40!”

It’s difficult to run your operations and stay at a

consistentRule of 40 output. Life just doesn’t work like that, especially if you skew heavily towards Q4

seasonality and an elongated enterprise sales

motion.

Takeaway: The Rule of 40 is a a general target to work to in the long

term, not something to nail period to period.

It’s a lowish bar

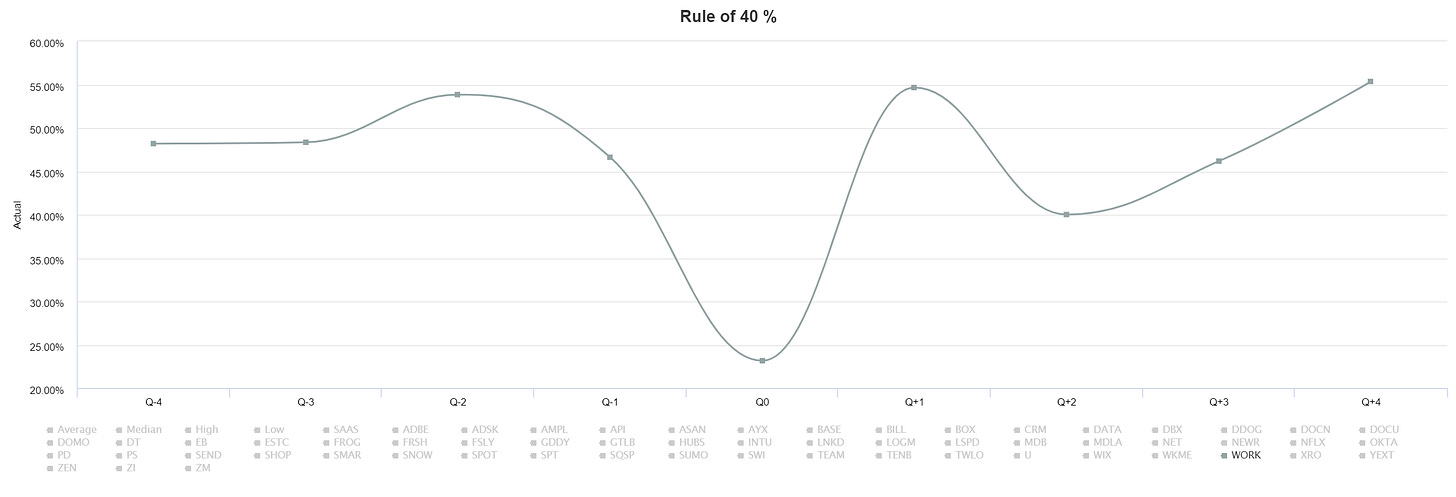

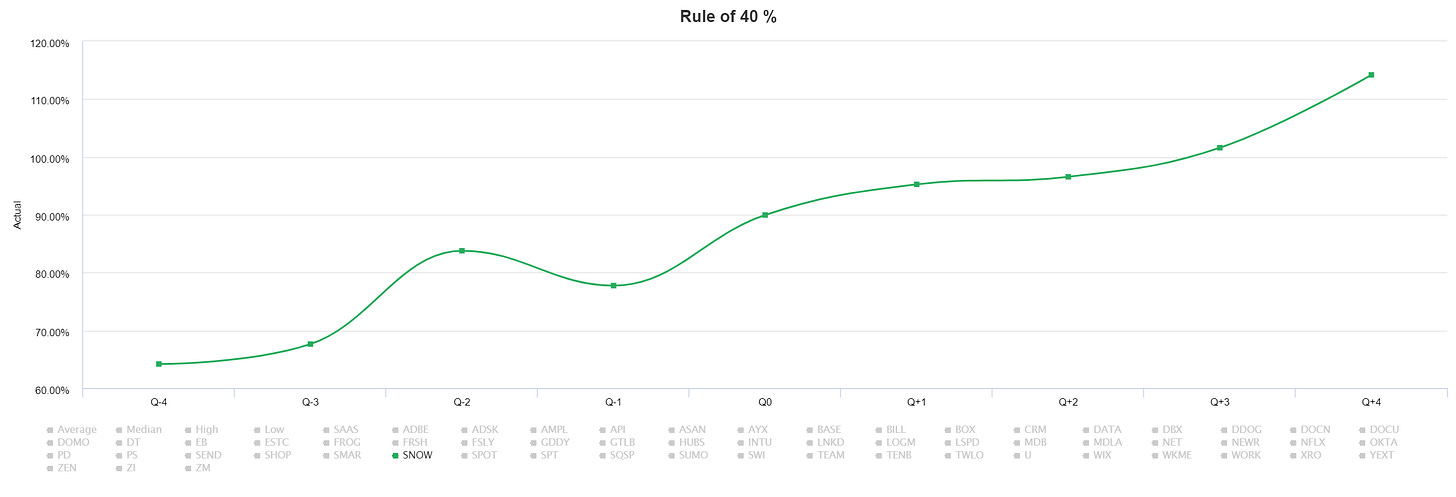

$SNOW Rule of 40

Peep Snowflake’s Rule of 40. They have every right to rename the metric the Rule of 60, since that’s where the Y axis starts. They were able to become efficient with scale, driving better bottom line margins at the same time their revenue grew leaps and bounds.

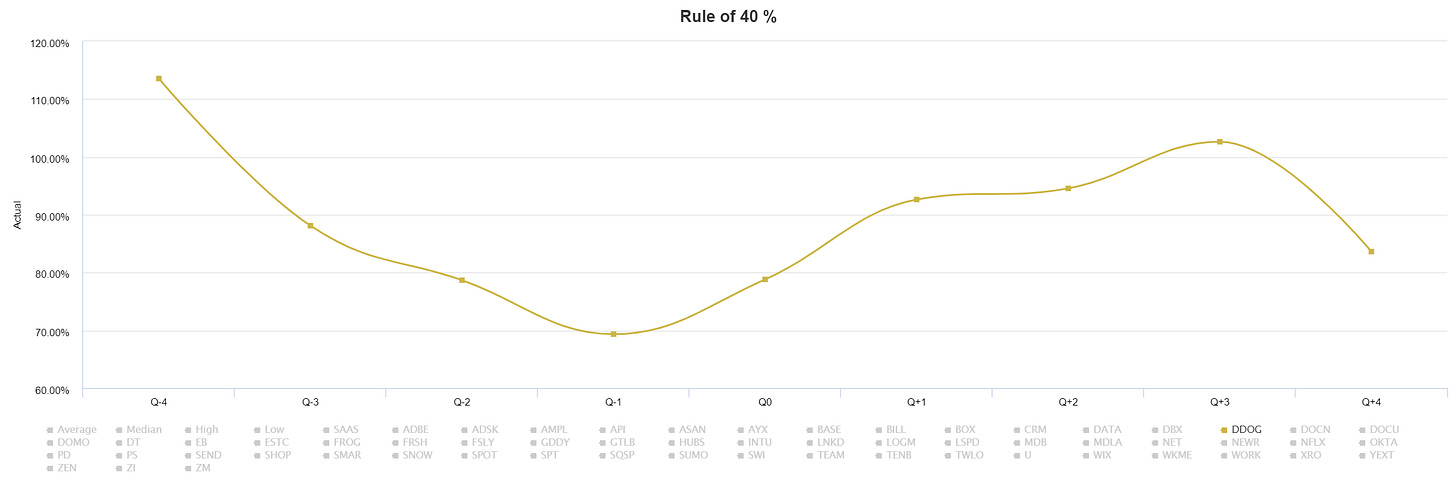

And here’s DataDog. It’s a similar story. The closest they come to 40% is 70%, a full 30% ahead of the “target”.

$DDOG Rule of 40

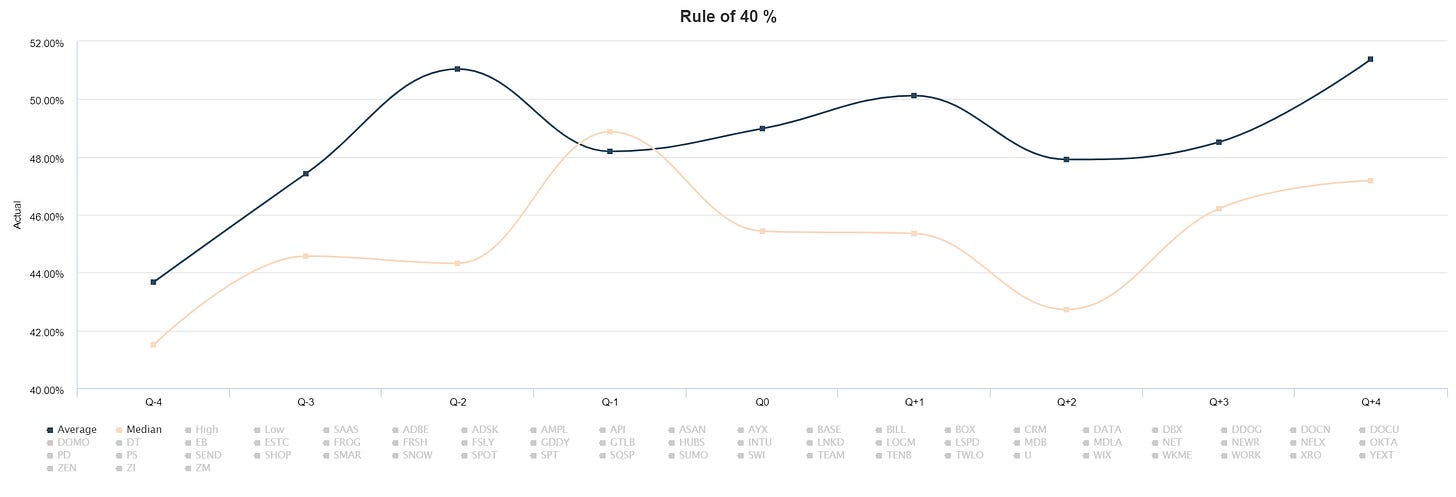

Finally, here’s the average and median across that cohort of 60 PLG SaaS companies.

PLG Average and Median Rule of 40

You can see the average is closer to 50% and median closer to 45%.

Takeaway: Hitting 40 is more average than excellent, and no one wants to

build an average company.

Conclusion

As OpenView explains,

Rule of 40 has always been a solid gut

check for the general balance of a company’s growth and profitability. However, it’s become increasingly important as a driver

of how businesses are valued. For earlier stage companies, Rule of 40 can vary widely from quarter to quarter. Achieving

40 each quarter is not required. But, it is required to have a grasp on what caused a drop or spike, and what can be done to

get to 40 long term.

I’d go a step further and amend the last phrase to: “what can be done to consistently operate above

40 in the long term.”

Maybe it makes sense for stock market pickers to use the Rule of 40 as a “sanity” check. But as someone responsible for making sure the trains

run on time, I don’t think the Rule of 40 is very useful, for all the reasons outlined above.

Agree? Disagree? Come tell us at the event on Thursday November 12th at 12 EST. When you register you’ll get

a copy of the report.

What I’ve Been Reading

Speaking of PLG… I was recently turned on to Top of the Lyne: Hard data. Deep research. Jaw-dropping insights. And the freshest memes. The art and science of product-led growth. Recommended by 7,000+ revenue leaders from Canva, Stripe, Notion, Figma, and 1,000s of other PLG companies.

Terms By accessing this web site, you are agreeing to be bound by these web site Terms and

Conditions of Use, all applicable laws and regulations, and agree that you are responsible

for compliance with any applicable local laws. If you do not agree with any of these terms, you

are prohibited from using or accessing this site. The materials contained in this web site are

protected by applicable copyright and trade mark law whether by Virtua Research Inc. or

others.

Use License Permission is granted to this site depending on level of permission. Research

is for personal consumption only unless otherwise permitted by agreement between Virtua and

user. This is the grant of a license, not a transfer of title, and under this license you may:

only modify or copy the materials to the terms of agreement;

not use the materials for any commercial purpose outside of research analysis, or for

any public display (commercial or non-commercial);

not attempt to decompile or reverse engineer any software contained on Virtua

Research's web site;

not remove any copyright or other proprietary notations from the materials; or

not transfer the materials to another person or "mirror" the materials on any other

server with out the specific permission of Virtua Research

This license shall automatically terminate if you violate any of these

restrictions and may

be

terminated by Virtua Research at any time. Upon terminating your viewing of these materials

or

upon the termination of this license, you may retain any downloaded materials in your

possession

whether in electronic or printed format only for continued personal use.

Usernames and passwords are authorized only to the subscribing members.

Sharing of user names

beyond the authorized users is strictly prohibited. Under no circumstances are passwords to

be

shared beyond authorized use.

Disclaimer The materials on Virtua Research's web site are provided "as

is". Virtua

Research

makes no warranties, expressed or implied, and hereby disclaims and negates all other

warranties, including without limitation, implied warranties or conditions of

merchantability,

fitness for a particular purpose, or non-infringement of intellectual property or other

violation of rights. Further, Virtua Research does not warrant or make any representations

concerning the accuracy, likely results, or reliability of the use of the materials on its

internet web site or otherwise relating to such materials or on any sites linked to this

site.

Research is provided, prepared and issued by Virtua Research Inc. and is

provided for

informational purposes only, and does not constitute an offer or solicitation to buy or sell

any

securities discussed herein in any jurisdiction where such offer or solicitation would be

prohibited.

Securities mentioned as part of this site in this site may not be

suitable for all types of

investors. This site and its associated research does not take into account the investment

objectives, financial situation or specific needs of any particular client and recipients

should

consider any research as only factors in making investment decisions. Recipients should not

rely

solely on investment considerations or recommendations contained herein, if any, as a

substitution for the exercise of independent judgment of the merits and risks of

investments.

Before making an investment decision with respect to any security

referred to on this site,

the

recipient should consider whether such investment consideration is appropriate given the

recipient's particular investment needs, objectives and financial circumstances.

Past performance is not a guarantee of future results, and no

representation or warranty,

express

or implied, is made regarding future performance of any security mentioned on this site. The

price of the securities mentioned on this site and the income they produce may fluctuate

and/ or

be adversely affected by exchange rates, and investors may realize losses on investments in

such

securities, including the loss of investment principal.

Virtua Research does not accept any liability for any loss arising from

the use of

information

contained on this site. Information, opinions and statistical data contained on this site

were

obtained or derived from sources believed to be reliable however Virtua Research does not

represent that any such information, opinion or statistical data as accurate or

complete.

All estimates, opinions and recommendations expressed herein constitute

judgments as of the date of publication and are subject to change without notice. Nothing on

this site constitutes legal, accounting or tax advice. Since the levels and bases of taxation

can change, any reference on this site to the impact of taxation should not be construed as

offering tax advice on the tax consequences of investments.

Limitations In no event shall Virtua Research or its suppliers be liable for any damages

(including, without limitation, damages for loss of data or profit, or due to business

interruption,) arising out of the use or inability to use the materials on Virtua Research's

Internet site, even if Virtua Research or a Virtua Research authorized representative has

been

notified orally or in writing of the possibility of such damage. Because some jurisdictions

do

not allow limitations on implied warranties, or limitations of liability for consequential

or

incidental damages, these limitations may not apply to you.

Revisions and Errata The materials appearing on Virtua Research's web site could include

numerical, technical, factual, typographical, or photographic errors. Virtua Research does

not

warrant that any of the materials on its web site are accurate, complete, or current. Virtua

Research may make changes to the materials contained on its web site at any time without

notice.

Virtua Research does not, however, make any commitment to update the materials.

Links Virtua Research has not reviewed all of the sites linked to its Internet web site and

is

not responsible for the contents of any such linked site. The inclusion of any link does not

imply endorsement by Virtua Research of the site. Use of any such linked web site is at the

user's own risk.

Site Terms of Use Modifications Virtua Research may revise these terms of use for its web

site

at any time without notice. By using this web site you are agreeing to be bound by the then

current version of these Terms and Conditions of Use.

Governing Law Any claim relating to Virtua Research's web site shall be governed by the

laws of the State of Massachusetts without regard to its conflict of law provisions.

General Terms and Conditions applicable to Use of a Web Site.

Privacy Policy

Your privacy is very important to us. Accordingly, we have developed this Policy in

order for you to understand how we collect, use, communicate and disclose and make use

of personal information. The following outlines our privacy policy.

Before or at the time of collecting personal information, we will identify the purposes

for which information is being collected.

We will collect and use of personal information solely with the objective of fulfilling

those purposes specified by us and for other compatible purposes, unless we obtain the

consent of the individual concerned or as required by law.

We will collect personal information by lawful and fair means and, where appropriate,

with the knowledge or consent of the individual concerned.

Personal data should be relevant to the purposes for which it is to be used, and, to the

extent necessary, for those purposes, should be accurate, complete, and up-to-date.

We will protect personal information by reasonable security safeguards against loss or

theft, as well as unauthorized access, disclosure, copying, use or modification.

We will make readily available to customers information about our policies and practices

relating to the management of personal information.

We are committed to conducting our business in accordance with these principles in order

to ensure that the confidentiality of personal information is protected and maintained