Don’t let the Rule of 40 rule your company

Why I think the Rule of 40 is lame

This Thursday I’ll be participating in a virtual event OpenView is putting on to roll out their 2022 SaaS Benchmarking Report. I’ve been a disciple of this report for +5 years, having built multiple annual operating plans off of the rich data set. To a CFO or FP&A professional in tech, it’s the holy grail of SaaS benchmarking.

Curt and Kyle at OV crunched the financial and operating metrics of 660 private SaaS companies so you don’t have to.

RSVP for the event and gain early access to the report here👇

In addition to the lucrative appearance fee I’ll be collecting, I also received early access to the data. While thumbing through it, their recent analysis on the Rule of 40 caught my eye. You may have heard of this metric – like the Undertaker, it’s risen from the dead during the latest tech market correction.

At the risk of ruffling some feathers, it’s time for me to come clean – I think the Rule of 40 is lame. Let’s dig into why.

Disclosure: OpenView did not actually pay me anything to participate, however, I did stop by their office for happy hour two weeks ago and enjoyed two (free) Miller Lites and one (free) cupcake.

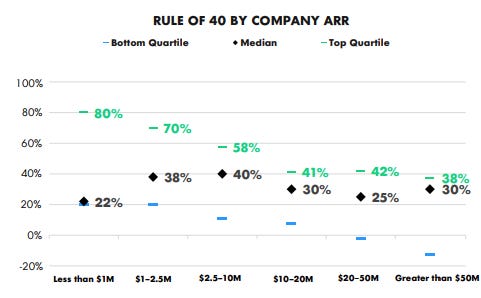

What’s the Rule of 40%?

The Art:

Trying to measure efficiency when you’re losing money can be a mixed bag of burritos. Some businesses raise a ton of money so they can prioritize growth at all costs (see: Gitlab). Other businesses are designed to run like a money printer, spitting out free cash flow and fat dividends for shareholders (see: Qualcomm).

But for many businesses, the truth lies somewhere in the middle. Some investors validate a “good” balance between growth and profitability by checking if revenue growth rate plus profit (or loss) rate exceeds 40%.

The Science:

Rule of 40 = YoY ARR Growth + LTM EBITDA Margin > 40%So, if you’re growing at 50% y/y and have a -15% EBITDA margin, your Rule of 40% = 35%…womp womp.

Where does the Rule of 40 go wrong?

I have four bones to pick with the Rule of 40:

- It ignores where you are in your business lifecycle.

- You can game it with superior growth.

- It’s a hard target to keep consistent in all periods, due to seasonality

- It’s a lowish bar if you want to be great.

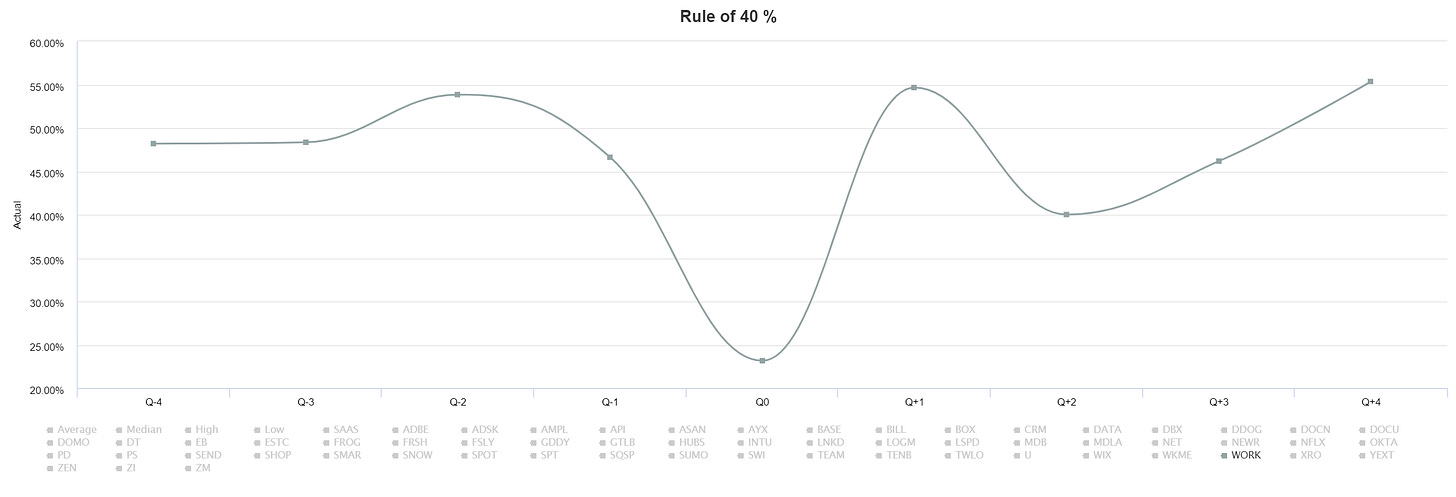

I took a trip in the way back machine using Virtua Research’s lifecycle analysis tool to stress test a cohort of companies in the four quarters leading up to (Q-4 through Q-1) and immediately preceding (Q+1 through Q+4) their IPO (Q0).

The research is based on a selection of 60 PLG companies, in honor of OpenView.

Here are my arguments against a dogmatic adherence to the Rule of 40:

Thanks for reading Mostly metrics! Subscribe for free to receive new posts and support my work.

It ignores where you are in your business lifecycle

WorkDay was a solid investment if you bought in when they went public, and maintains a strong financial profile to this day. However, their Rule of 40 took a major dip at time of IPO as they made some investments in the business to scale.

Nonetheless, their stock price jumped 72% on day of IPO. If you religiously followed the Rule of 40 you would have dumped them, and kicked yourself down the road.

There are times to step on the gas pedal and say damn the torpedoes. There are also times to get to an efficient P&L in a hurry. Just because you are in one season rather than another doesn’t mean you are necessarily a “bad” company.

Takeaway: Not all periods are the same. And not all periods should be 40%.

You can game it by going big on just growth

I also think there are diminishing returns past a certain growth rate. Investors aren’t necessarily going to pay any extra for 125% growth vs 110% growth if you are losing 50% per year.

However, adhering to the Rule of 40 in a bubble would give you the vote of approval on growth of 140% and losses of 100%. Talk about false signals.

Takeaway: Not all growth percentage points are created equal.

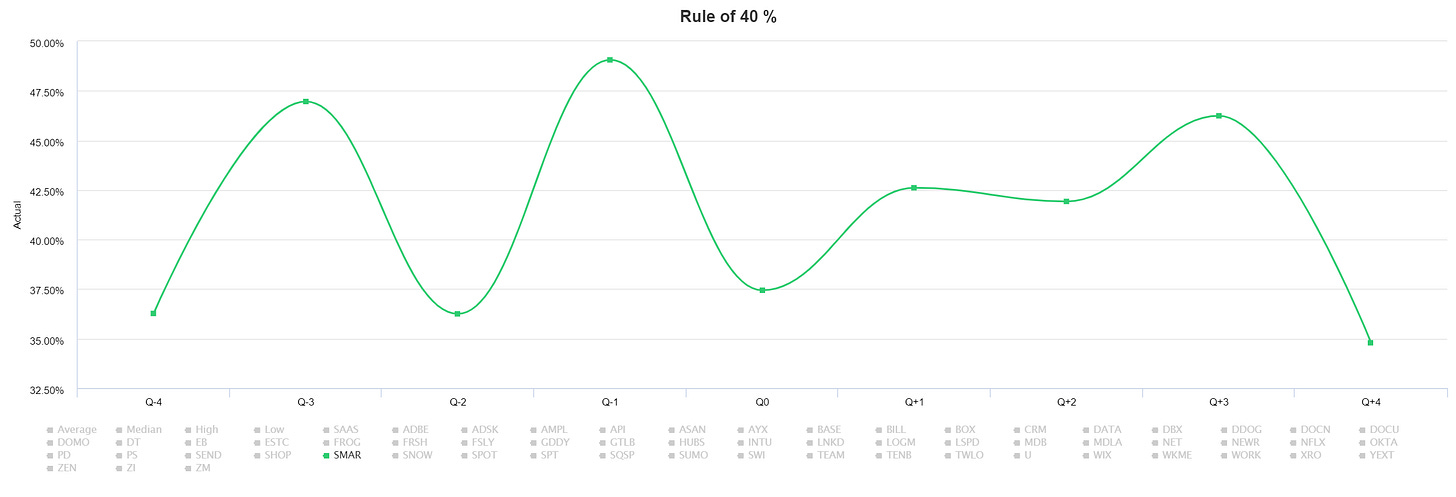

It’s a hard target to keep consistent in all periods, due to seasonality

Here’s SmartSheet. They oscillate between a low of 35% and a high of 48%. It looks like one of those Inflatable Whacky Willys at the used car markets.

I highly doubt when they touched 35% their CEO yelled “HALT THE PRESS! We must get back to 40!”

It’s difficult to run your operations and stay at a consistent Rule of 40 output. Life just doesn’t work like that, especially if you skew heavily towards Q4 seasonality and an elongated enterprise sales motion.

Takeaway: The Rule of 40 is a a general target to work to in the long term, not something to nail period to period.

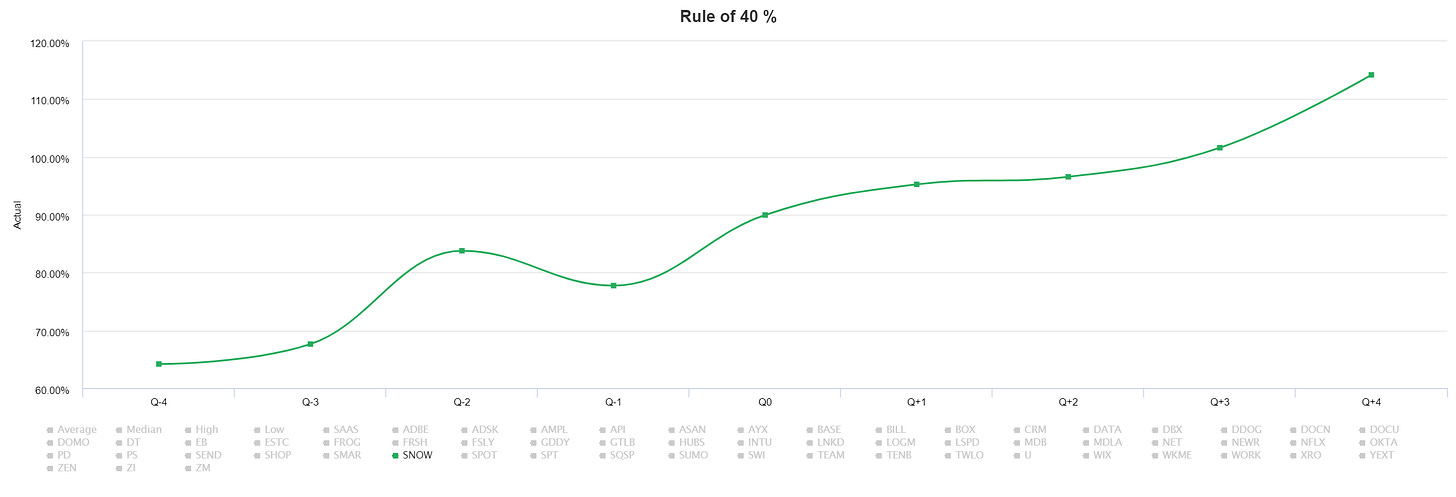

It’s a lowish bar

Peep Snowflake’s Rule of 40. They have every right to rename the metric the Rule of 60, since that’s where the Y axis starts. They were able to become efficient with scale, driving better bottom line margins at the same time their revenue grew leaps and bounds.

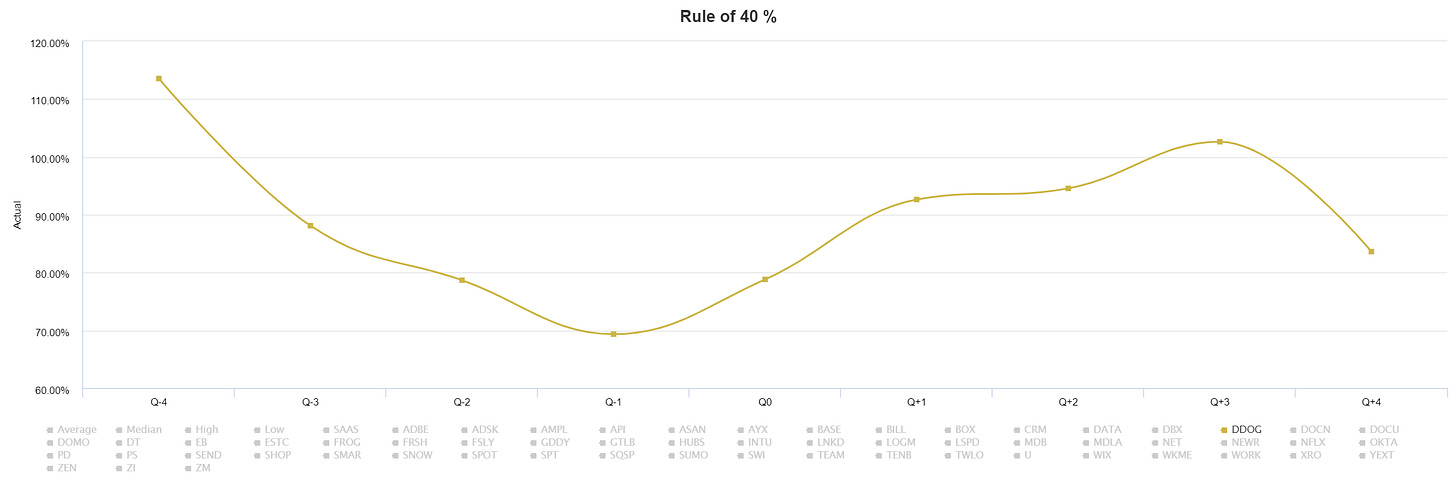

And here’s DataDog. It’s a similar story. The closest they come to 40% is 70%, a full 30% ahead of the “target”.

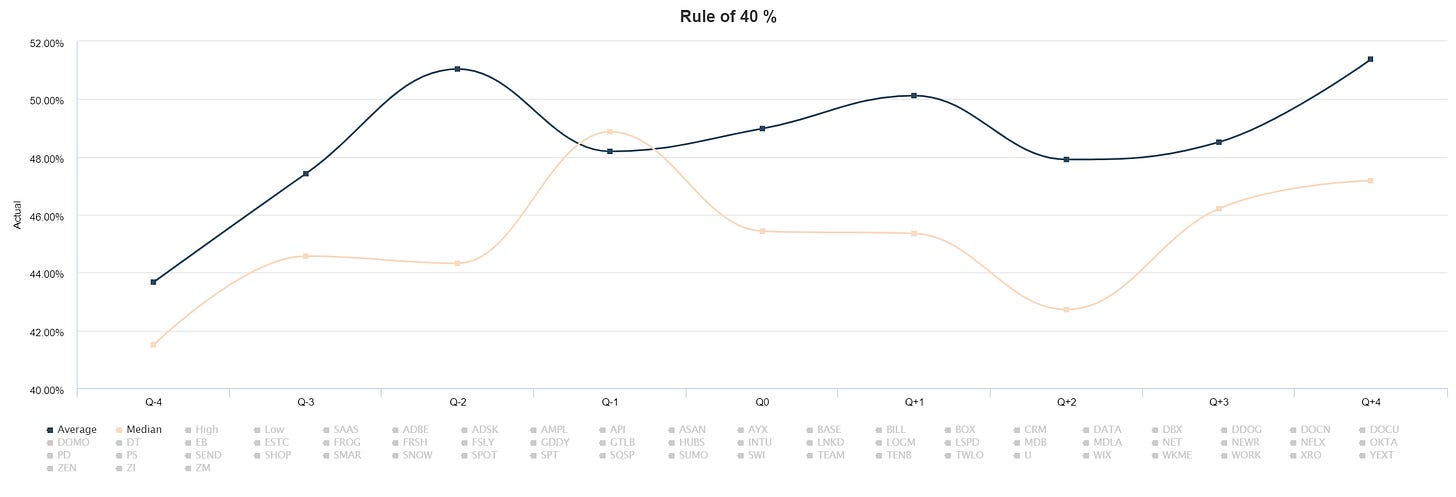

Finally, here’s the average and median across that cohort of 60 PLG SaaS companies.

You can see the average is closer to 50% and median closer to 45%.

Takeaway: Hitting 40 is more average than excellent, and no one wants to build an average company.

Conclusion

As OpenView explains,

Rule of 40 has always been a solid gut check for the general balance of a company’s growth and profitability. However, it’s become increasingly important as a driver of how businesses are valued. For earlier stage companies, Rule of 40 can vary widely from quarter to quarter. Achieving 40 each quarter is not required. But, it is required to have a grasp on what caused a drop or spike, and what can be done to get to 40 long term.

I’d go a step further and amend the last phrase to: “what can be done to consistently operate above 40 in the long term.”

Maybe it makes sense for stock market pickers to use the Rule of 40 as a “sanity” check. But as someone responsible for making sure the trains run on time, I don’t think the Rule of 40 is very useful, for all the reasons outlined above.

Agree? Disagree? Come tell us at the event on Thursday November 12th at 12 EST. When you register you’ll get a copy of the report.

What I’ve Been Reading

Speaking of PLG… I was recently turned on to Top of the Lyne: Hard data. Deep research. Jaw-dropping insights. And the freshest memes. The art and science of product-led growth. Recommended by 7,000+ revenue leaders from Canva, Stripe, Notion, Figma, and 1,000s of other PLG companies.

Quote I’ve Been Pondering

“If you can fill the unforgiving minute

With sixty seconds’ of distance run,

Yours is the Earth and everything that’s in it…”

-Rudyard Kipling, If